Getting an IRS notice about unpaid taxes can be worrying. You see the words levy and garnishment and wonder what they mean. They are different collection tools, and knowing the difference helps you protect your money.

Ignoring the IRS will not make the problem go away. The agency has steps to follow before taking enforcement action, but those steps move quickly. When you know what levy and garnishment mean, you can respond faster.

What Is an IRS Levy?

An IRS levy lets the agency take your property to collect unpaid taxes. This is a serious action. Unlike a tax lien which is just a claim against your property, a levy actually takes the money or property to pay what you owe.

The IRS usually uses a levy after you ignore several notices or fail to make a payment plan. Before taking action, the agency sends a final notice. From there, you have 30 days to respond before the IRS moves forward.

The IRS can take many types of assets through a levy, including:

- Money in your bank accounts

- Your federal and state tax refunds

- Business equipment and customer payments

- Social Security benefits

Through the Federal Payment Levy Program, the IRS can take up to 15% of your Social Security benefits. The agency uses Form 668-A for bank levies and Form 668-W for wage garnishments. Once the 30-day period ends, the IRS can take the property.

What Is IRS Wage Garnishment?

A wage garnishment takes money straight from your paycheck. To start this process, the IRS contacts your employer and asks them to hold back a portion of each paycheck. From that point on, your employer sends that money to the IRS until your tax debt is paid.

This levy keeps going until your debt is cleared, the collection time runs out, or you set up a payment plan with the IRS. The amount taken depends on your filing status, how often you get paid, and how many dependents you claim.

A bank levy on the other hand freezes your account once and takes whatever money is in it at that moment. Taxpayers therefore need effective ways to stop irs wage garnishment and protect their income before the financial pressure becomes too much.

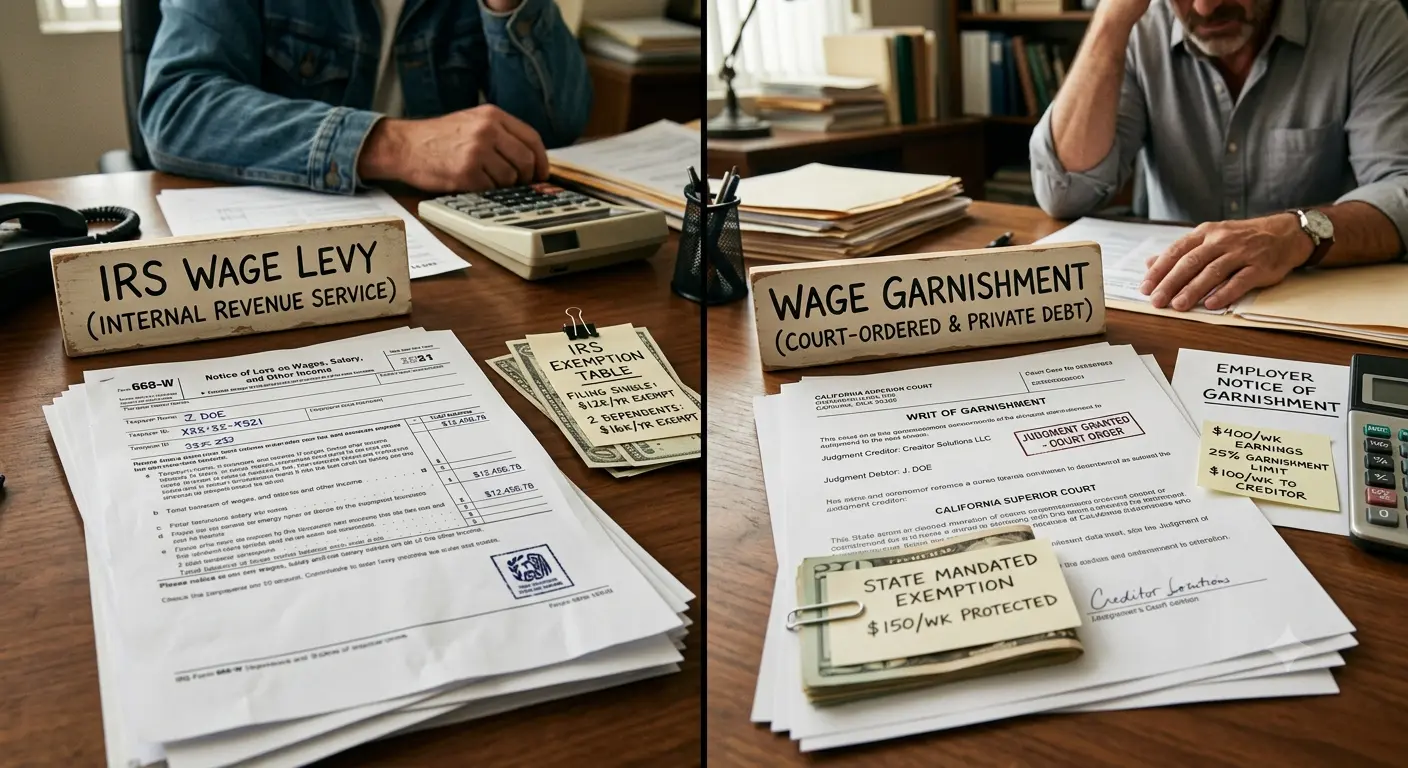

IRS Wage Levy vs Wage Garnishment: Key Differences

The following subsections break down the five most important differences between these enforcement actions.

| Aspect | Wage Garnishment | IRS Wage Levy |

|---|---|---|

| Assets Affected | Targets only a portion of an employee’s wages, salary, bonuses, commissions, and other compensation through employer withholding | Reaches well beyond payroll to include bank accounts, retirement accounts, vehicles, real estate, and other types of property |

| How Long Collections Continue | Stays in place until the debt is fully paid, the levy is released, or the collection time limit runs out | Generally a one-time seizure of funds available at that moment, though the IRS can issue additional levies if the debt remains |

| Notice Requirements | Requires advance written notice with a Final Notice of Intent to Levy (Letter 1058 or LT11) sent at least 30 days before action | Same notice requirements as garnishment; taxpayers receive several reminder notices before the final warning |

| Financial Impact | Creates an ongoing reduction in take-home pay every pay period until settled; monthly budgeting becomes harder but more predictable | Causes a sudden loss of funds by freezing accounts immediately; banks hold money for 21 days before sending to the IRS, offering a short window to negotiate |

| Available Resolution Options | Payment plans, settlement offers, temporary hardship status, formal hearing requests, and levy release requests based on financial difficulty | Same resolution options available as garnishment |

Can You Stop an IRS Levy or Wage Garnishment?

Yes, you can stop an IRS levy or wage garnishment, but you must act quickly. The sooner you respond, the more options remain available. Below are the most common ways to stop a levy or garnishment and take back control of your money.

Installment Agreements

An installment agreement lets you pay your tax debt over time in monthly payments. Once the IRS approves this plan, it will usually release the levy or garnishment. You can apply online, by phone, or by mailing Form 9465. The IRS offers different payment plans based on what you owe and your financial situation.

Offer in Compromise

An Offer in Compromise allows you to settle your tax debt for less than what you owe. This option works best when you cannot pay the full amount or when paying it would cause serious financial trouble. The IRS reviews your income, expenses, property value, and what you can afford to pay. Approval is not assured, but it can bring major relief if the IRS accepts your offer.

Currently Not Collectible Status

Currently Not Collectible status briefly puts IRS collection efforts on hold. The IRS gives this status when your monthly income does not cover your basic living costs. During this time, the levy or garnishment stops. Keep in mind, though, that interest and penalties keep adding up. The IRS may also place a federal tax lien to protect its interests.

Filing Missing Tax Returns

The IRS will not stop a levy or garnishment if you have not filed your tax returns. In fact, filing all late returns is a must before any resolution can move forward. After you file, the IRS can figure out your total balance and choose the best collection option for your case.

Professional IRS Representation

Working with a professional representative can make a noticeable difference in stopping a levy or garnishment. It remains a fact that a tax resolution specialist assists you in gathering the right paperwork and presenting your case in the best light.

When Should You Seek Professional Tax Resolution Help?

You do not have to deal with the IRS by yourself. Many taxpayers gain from professional support during the collection process. In fact, seeking help from a tax resolution cpa early can stop enforcement actions and lower your stress. You should think about reaching out to a professional if any of these apply to you:

- You have gotten multiple IRS notices and are not sure how to reply

- A bank or wage levy is already happening or you have received a warning

- You owe a large tax balance that you cannot afford to pay off

- You have business tax problems involving payroll or excise taxes

- You feel confused or uncertain about which choice is right for you

How Professional Representation Can Help Protect Your Rights

Dealing with the IRS can be scary, but you do not have to go through it alone. A trusted tax attorney grand rapids mi helps you in:

- Going over IRS letters and telling you what they mean

- Checking which relief programs work best for you

- Talking to the IRS directly so you do not have to

- Putting together a plan that fits your unique situation

Taking Control of Your Tax Situation

Knowing the difference between an IRS levy and a wage garnishment is the first step to protecting your money. Both are serious, but each one works differently and needs a different response. Always remember that acting fast gives you more choices and better results. Whether you pick an installment agreement, an offer in compromise, or currently not collectible status, the main thing is to act before the IRS moves ahead. If you are not sure which way to go, professional tax resolution services can help you through it. You do not have to face the IRS by yourself.